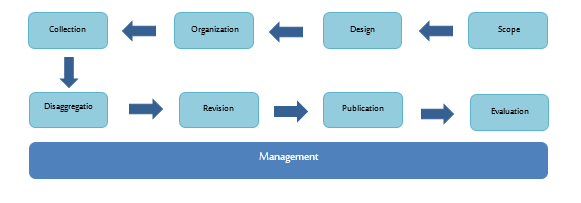

Introduction

First: Scope stage

Second: Design stage

Third: Organization stage

Fourth: Collection stage

Fifth: Disaggregation stage

Sixth: Revision stage

Seventh: Publication stage

Eighth: Evaluation stage

Ninth: Management stage

Introduction:

GASTAT implements all its statistical works in accordance with a unified methodology that compile with the nature of each statistical product. It relies on the Manual of the Statistical Procedures which conforms with the procedures adopted by the international organizations. The statistical product goes through eight connected stages, in

addition to a ninth stage (the comprehensive "management" stage), which are as follows:

The first three stages (Scope, design, and organization) are collaborative stages between GASTAT and its clients from the different developmental entities. However, the fourth stage (Data collection) is a collaborative stage between GASTAT and the statistical community either households or establishments, in order to complete data and information. On the other hand, the rest of the stages are considered statistical stages carried out by GASTAT, including (Disaggregation, revision, and publication). After that, the eighth stage (Evaluation) is done through collaboration with clients again, whereas the (Management) stage is an administrative and organizational stage that is connected with all stages. These stages have been applied to prepare the National Accounts Statistics as follows:

First stage: The scope

The first step in the process of producing (National Accounts Statistics), it is also the first collaborative stage between GASTAT and a number of relevant governmental and private sectors, and the concerned departments inside GASTAT such as the department of industry and businesses, the department of external trade, and the department of Prices statistics, in addition to the governmental entities such as the Ministry of Finance, SAMA, and Ministry of Energy, Industry and Mineral Resources in order to identify the nature of statistics that can be provided through the administrative records of these entities. They are also necessary to determine GASTAT needs and requirements to guarantee achieving the objectives of the National Accounts Statistics Bulletin, which can be summarized as follows:

• Supporting decision and policy makers, researchers, and those who are interested in getting up-to-date and comprehensive statistics related to the national accounts in accordance with the most recent international regulations.

• Providing estimates of GDP in (current and constant prices) for the current fiscal year, that show the expenditure on GDP and measure the contribution of the different institutional sectors and economic activities in GDP.

• Providing updated economic indicators such as GDP growth rates, and the contribution of the different institutional sectors and economic activities in GDP

• Providing revised data on GDP in (current and constant prices) for the past fiscal year.

• Providing indicators on available income and its distribution between saving and consumption.

• Providing many analytical tables that highlight the national economy tracks such as GDP growth rates, GDP components, and the interrelations among the major economic aggregates.

At this stage, the statistics to be published were verified to make sure it meets the requirements of the Saudi Vision 2030, in addition to its coverage of regional requirements such as (the Statistical Center of GCC countries), Arab Monetary Fund, Arab League, and some international requirements represented in the United Nations Economic and Social Commission for Western Asia (ESCWA), the World Bank, and the International Monetary Fund.

Second stage: The design

The stage of designing the statistical work as it is considered a whole product. Through this stage, data collection methods and tools are identified. Clients collaborate in all these procedures to benefit from their feedbacks, so that all requirements can be achieved within the statistical product.

The most important outputs of this stage are:

1. Statistics sources:

The national accounts statistics depend on the administrative records data of governmental entities and related establishments. GASTAT calculates the indicators of these intities and publish them through the National Accounts Statistics Bulletin.

Administrative records refer to all data and information that are recorded and updated by the related governmental entities and resulted from the official documentation operations which these entities follow.

2. Determining the required data from the administrative records and the way they are estimated:

GASTAT completed all necessary basic data that are related to the national accounts statistics of governmantal entities as follows:

1. Organizational sectors:

Bellow are the most important organizational economic sectors in Saudi Arabia, to understand each sector, in addition to its data type and coverage.

(A) Business sector (industries):

This sector includes all the productive economic units that produce commodities and services to be sold in the market with a price that aims to cover the production costs. These units may also produce these commodities and services to be used personally in all economic activities according to ISIC4 .

This sector also includes:

1. Governmental non-financial productive authorities and projects:

This includes all governmental productive economic units that produce commodities and services either to be sold in the market with a price that aims to cover the production costs, or with a less price that resulted from the government policy in declining prices. These units may also produce commodities and services to be used inside the governmental productive and administrative organizations.

2. Non-financial joint projects:

These include all resident economic units producing goods and services which are sold in the market at a price that covers production cost. The government shares the property of the capital of these units with individuals and companies.

3. Non-financial private corporations

This sector includes all resident productive units owned and administered by the private sector. It is divided into two sections:

3.1. Institutional projects

They are the projects with independent bookkeeping and financial accounts such as joint-stock companies, companies limited by shares, limited-liability companies, simple limited partnerships, collective companies, large individual enterprises with financial accounts separated from the owner of the enterprise, and branches of foreign companies.

3.2. Non-institutional projects

They include small individual projects which do not have independent bookkeeping or accounts and whose financial transactions are difficult to be separated from the owner of the enterprise.

4. Financial corporations

They include the financial bodies primarily dealing with financial transactions in the market, and those related to financial rights and commitments, in addition to insurance companies.

This concept also comprises Saudi Arabian Monetary Agency (SAMA), the various development funds, commercial banks, insurance companies, and other financial institutions and authorities.

(B) Producers of Govt. services

These include all ministries and government agencies working in the field of administration, defense, public security educational, cultural, entertainment, development services and other collective services aimed at community development. They also include government units specialized in providing the repetitive services such as issuance of passports, licensing, and driving licenses, notwithstanding the fact that payments for these services may not cover the current costs of administering these units.

(C) Household sector

This sector covers all individuals and households residing within the Saudi territory for more than one year. They might be Saudis or non-Saudis . It also includes non-profit private institutions serving households such as (charities), sports clubs and the likes.

(D) The rest of the world sector

This sector has to do with the Kingdom's transactions with the rest of the world so far as visible and invisible exports and imports and all financial and capital transactions which lead to creating financial rights and commitments for the Kingdom with the rest of the world.

2. Estimation Methods

A. Estimates at current prices:

Following are the methods used in the economic activities to estimate production, intermediate consumption, value added wages and salaries (compensation of employees, operating surplus and capital formation elements.

Agriculture and fishing:

This includes plant production, animal production, fishing, and honey production... etc. Estimations are based on the results of the economic research carried out by GAStat annually and on the data obtained from the Ministry of Environment, Water and Agriculture. They are derived from the results of censuses and agricultural research conducted by the ministry, and they provide data on production, intermediate consumption, value added, paid wages, operating surplus, and capital formation.

Crude petroleum and natural gas

Estimations are conducted according to the information received by GAStat from the petroleum companies working in KSA, through the Ministry of Energy, Industry and Mineral Resources.

Mining and quarrying

The estimation of the value of production and other elements such as intermediate consumption, value added, wages and salaries is based on the results of the economic research conducted by GAStat.

Manufacturing:

Manufacturing covers the following subactivities:

• Manufacture of food products and soft drinks

• Manufacture of textiles, garments and leather

• Manufacture of wood and wood products including furniture

• Manufacture of paper, paper products, printing and publishing

• Manufacture of chemicals, chemical products, petroleum, coal, rubber, and plastic products

• Manufacture of non-metallic minerals-except petroleum and coal products

• Manufacture of basic metals

• Manufacture of metal products, machinery and equipment

• Other

The different economic aggregates related to production and capital component formation are measured according to this classification and to the information provided by economic research conducted by GAStat in this regard.

Electricity, gas and water:

The estimation of the costs of different production elements and capital formation is made depending on the data provided by the economic researches conducted by GAStat covering the Saudi Electricity Company, National Manufacturing and Gas Company, and water sources and distribution (National Water Company).

Construction:

This sector covers all building processes (of housing and non-housing buildings alike) as well as road construction and pavement, and construction of bridges, tunnels and railways, in addition to water, sewage, electricity, and telecommunication utilities. This sector covers, over and above, drilling wells, reclaiming land, installing air-conditioning devices, connecting buildings to a water supply and sewerage network, as well as installing sanitary ware and elevators, aside from demolishing buildings, etc.

The adopted estimation approach for this activity leverages a myriad of diversified methods. For example, national accounts variables are estimated according to the results of the economic researches and other sources such as annual final accounts and reports of data sources regarding the expenditure on new fixed assets by type of each asset.

Wholesale and retail trade, restaurants and hotels:

Estimations of this sector depend on the data provided by the periodical economic researches conducted by GAStat in the field of statistics of distribution trade and purchases value services, sales value, paid wages and salaries, newly purchased fixed assets and all types of expenditure and other revenues. The production in the field of wholesale and retail trade is estimated as the difference between the value of sales and purchases of goods purchased to be sold without any change whether in form or in content. The production of restaurants and hotels is estimated by revenues for providing meals, accommodation, and hospitality services. Also, the imports are used as an indicator in completing the estimates of wholesale and retail trade, while number of occupied rooms, number of residents, and total revenues are used as an indicator so far as hotels are concerned.

Transportation, communication and storage:

This sector covers all various units performing the services of this activity such as land, air and maritime transportation, storage, mail and telecommunication services... etc. It depends on the data provided by periodical economic researches conducted by GAStat, which cover the institutions working in this field.

Finance, insurance, real estate and business services:

The economic researches conducted by GAStat periodically are considered the source of information required for the estimation. And since such data cover private sector only, other data, provided at financing funds and the monetary institutions, are used to complete the framework of this sector. Besides, household expenditure and income survey is used to estimate the value of housing buildings rental, whether paid or measured, i.e. whether these buildings are rented to others or inhabited by their owners.

Social and personal services :

The periodical economic researches conducted by GAStat play a key role in providing information required for estimating production, intermediate consumption, paid wages and salaries, value added, capital formation components (new fixed assets purchased by asset type) and the rest of property income terms, in addition to using household expenditure and income to estimate the value of home services provided for households between themselves.

Producers of government services:

The government budget and the budgets affiliated to it, independent budgets, and the final account are considered the main source of data used in getting different economic aggregates. The government budget differs from the other regular budgets of companies in the method of preparation and classification, as it is divided into four sections:

Section I:

It deals with the expenditure on wages and salaries due to be paid for the employees.

Section II:

It focuses on operating expenditure (rewards, travel expenses, rentals, electricity and water charges, consumer materials and equipment, and subsidies).

Section III:

It deals with expenditure on maintenance and operation.

Section IV:

It deals with various government investments aspects (spent on projects).

As the government final accounts are classified in accordance with financial classifications, National Accounts Department modifies this classification to economic classifications. According to the UN sysytem, government production is the sum of expenditure on government employees wages and salaries, current expenditure on goods and services, consumption of capital and net indirect taxes. The expenditure is classified by different functional classification aspects (public services, defense, education, health, social insurance and welfare services, housing and community development, other collective and social services, economic services, other purposes).

(B) Estimations at constant prices

The year 2010 is the base year used for calculating estimations of the national accounts at constant prices. There are different confirmation methods varying from one economic activity to another according to the available information. Following are the methods used in constantprice estimations:

Agriculture and Fishing :

The index of production quantities (plant, animal, and fish production) was used for calculating the product value at constant prices.

Crude oil and natural gas:

Given that produced quantities are provided in barrels, the estimation is conducted depending on the index of those quantities.

Oil refining:

Depending on the availability of the refined product, a quantitative index was created to conduct constant-price estimations.

Other transformative industries:

The index of wholesale prices of those products is used to conduct constant-price estimations.

Electricity, gas and water:

Estimations are conducted depending on the index of sold quantities.

Construction:

The index of wholesale prices of building materials is used to conduct those estimations.

Wholesale and retail trade, restaurants and hotels:

The general index of wholesale and retail prices, restaurants and hotels is used to conduct estimations separately from one another.

Transport and Communications:

Estimations are made at constant prices using the index of transport and communication prices.

Banking services:

An implied index of the GDP (with the financial services excluded) is used in reestimating the current prices compared to the constant prices.

Rentals (of buildings):

The index of the cost of living of rentals is used to calculate the estimates at constant prices.

Social, collective and personal services:

The index of the cost of living was used in reestimating the numbers at current prices to figures at constant prices.

3. Terminologies and concepts that are related to the National Accounts Statistics:

• Gross Output:

The value of goods and services resulted from producing activity for institutional units that useinput during the accounting period. It includes finished, unfinished and the products produced for own use. The value of output is usually estimated at producer prices, that represents the market value at factory gate.

• Gross Domestic Product ( by production approach)

The total value added of the resident producers at producer price,in which customs fees or output totals are added and the total intermidate consumption are deducted and the net products taxes are added (taxes- subsidies ),which are not included in the outputs value.

• Gross Domestic Product ( by expenditure approach)

The total of final expenditure at purchasers price including exports at free on board prices (FOB), from which imports are deducted

• Gross Domestic Product ( by cost structure approach)

Total compensation of employees, net taxes, operating surplus and depreciation of fixed capital.

• National income

It is the GDP minus the preliminary incomes paid to the unestimated units, plus the preliminary incomes received from the unestimated units.

• Compensation of employees

Compensations are the total sums, in cash or in kind, payable by enterprises to employees in return for work before deducting premiums of social insurance, taxes, etc.

• Disposable income

It is the national income at market price, plus net current transfers from abroad.

• Intermediate Consumption

It is the value of goods and services that is used as inputs for the production process excluding constant assets as their consumption is considered as a consumption of the constant capital. The used goods and services might be totally transformed or consumed in the production process. Some inputs may emerge again after being transformed or merged with the outputs. There are some inputs that can be totally disappeared such as electricity and other similar services.

• Operating surplus

It is the added value minus the value of employees' remunerations, net indirect taxes, and the depreciation of fixed capital.

• Indirect taxes

The term refers to the taxes imposed on producers for producing, selling, buying, or using goods and services. Indirect taxes are usually added to production costs, and include customs fees.

• Production subsidies

They include grants payable by the government to the current account of private and public sectors, and grants offered by public authorities to government projects to compensate the loss resulting from a governmental policy aiming to keep price at a certain level. They may be measured as the difference between the target price and the actual market price paid by the purchaser.

• Depreciation of Fixed Capital

It represents the decrease of the constant assets value, used in production, during the accounting period as a result of a slump, obsolescence, or any deterioration factor. This depreciation could be deducted from the constant capital formation to get the net constant capital formation

• Net indirect taxes

They are the value of indirect taxes minus the value of production subsidies.

• Financial intermediation services indirectly measured

It is the difference between interest value and profits payable to banks and financial institutions on the one hand, and the value of interests payable to depositors on the other hand.

• Marketable goods and Services

The term refers to the value of goods and services which are sold in the market, or which are primarily manufactured to be sold in the market at a price intended to cover production cost. They include all goods and services domestically produced or imported from abroad, except the direct purchases from abroad by the government and the households.

• Non-marketable goods and Services

The term refers to the value of other goods and services which are offered at a price that does not usually cover production cost (for free or at a nominal price). Most of them consist of the production of government services producers and non-profit institutions serving households.

• Trade margin

A trade margin is the difference between the actual or imputed price by the purchaser for a commodity purchased for resale (either wholesale or retail), , and the price that would have to be paid by the distributor for the commodity at the time it is sold or used. The outputs of wholesale and retail trade are measured by the sum of trade margin values realized on the goods purchased for resale.

• Imports of Goods and Services Imports

It is the value of goods that have been transferred from being owned by non- residents to being owned by residents in Saudi Arabia. Moreover, the imports include the services provided by nonresidents to residents in Saudi Arabia. The imports include, the goods that cross the boards for processing. and the goods that prepared in foreign ports and transported by local transporters, nonmonetary gold. The import services include tourism and transportation services, communication, insurance, construction, financial services, royalties, licenses fees, personal and cultural services, and non-classified government services.

• Exports of Goods and Services Exports

It is the value of goods that have been transferred from being owned by residents in Saudi Arabia to being owned by non-residents. The exports include exported goods for processing, goods purchased in local ports by non-residents transporters, and nonmonetary gold. However, the exports of services include all services provided to non-residents such as tourism and transportation services, communication, insurance, financial services, royalties, licenses fees, personal, cultural, and recreation services, and government services.

• Government Final Consumption Expenditure

The value of the total goods and services that consumed by the government in the process of producing the government services. It equals the value of the government total production minus the value of the market and non- market sales. The government production value equals the intermediate consumption of goods and services in addition to the value of the compensation of employees, depreciation of fixed capital, and indirect taxes.

• Households Final Consumption Expenditure

The value of resident households final consumption expenditure on goods (durable and non-durable) and services minus their sales of used goods.

• Final Consumption Expenditure of NPISHs

The value of the NPISHs final consumption expenditure on goods and services that are provided free or at nominal price to households. This equals the value of production minus market and non- market sales.

• Private Final Consumption Expenditure

The value of final consumption expenditures of resident households and the NPISHs.

• Gross Fixed Capital Formation

The values of the net addition of the producers to the fixed assets minus the value of fixed assets disposed of by producers (additions - exclusions) (additions – eliminations) during the accounting period. In addition to additions made to non-productive assets such as land improvement, forest development, implantations and groves …etc. These additions are used for more than one year. They include changes in live-stock such as dairy livestock …etc. They also include transferring (sales and purchases) property costs regarding lands, forests, and mines …etc.

• Change in Stock

The market value of change that occurs during the accounting period of stock including raw material, product in process, finished products, animals for slaughtering, and purchased goods for resale. This represents the difference in the stock value at the end and at the beginning of the accounting period.

• Gross Capital Formation

It equals the value of fixed capital formation in addition to the change in stock.

• Constant assets

They are productive assets repeatedly or continuously used in production operations for a period of time exceeding one year. The fixed assets do not only include machinery and equipment, but also include different assets such as trees and animals which are repeatedly or continuously used for the production of other products, such as fruits and dairy products. Also, they include intangible assets such as computer software and artwork used in the production.

• Property income

It is the income received by the owner of unproductive financial or tangible asset for providing money or for putting the unproductive tangible asset at the disposal of other institutional unit. The financial instrument usually determines the terms and conditions of property income payment. Property incomes include interests, profit distribution, distributed shares, withdrawal from the income of quasicorporation, revenues of reinvested direct foreign investment, and property income payable to insurance policy holders as well as revenues.

• Interest

It is a form of property income that is received by the owners of specific types of financial assets such as deposits, securities other than shares, loans and other creditor accounts. The interest is defined as the sum that the debtor is liable to pay to the creditor over a given period of time by virtue of terms and conditions of the financial instrument agreed upon by debtor and creditor, without decreasing the value of the original debt.

• Shares

The term refers to the value of income payable for shareholders as a result of putting their money at the disposal of companies. It is a type of property income.

• Rental

It is the net rental value payable as a result of the exploitation of agrarian lands for the purpose of agriculture as well as the revenues of in-ground assets. It may be paid in cash or in kind. It is one of the forms of property income.

• Current transfers

The term refers to the value of transfers made between the dealers in the form of non-capital transfers.

4. Used Statistical Classifications:

Classification is defined as an organized group of related categories which are used to collect data according to similarity. Classification is the base for data collection and dissemination in various statistical fields, such as: (economic activity, products, expenses, occupations or health…. etc). classifying data and information helps to put them in meaningful categories to produce useful statistics. In fact, data collection requires an accurate organization and based on their common features to create reliable and comparable statistics. On the other hand, national accounts statistics are based on the international standards of data collection and classification and rely on the following classifications:

1. The National Classification of Economic Activites (ISIC4)

It is a statistical classification that is based on the unified international industrial classification of all economic and productive activities. it can be defined as (all the works and services practiced or provided by the establishments whether these services have achieved a financial return or not as in the case of charity institutions which mainly depend on donations.

2. Central Products Classification (CPC2)

It constitutes a complete product classification covering goods and services. It serves as an international standard for assembling and tabulating all kinds of data requiring product detail, including statistics on industrial production, domestic and foreign commodity trade, international trade in services, balance of payments, consumption and price statistics and other data used within the national accounts. It provides a framework for international comparison and promotes harmonization of various types of statistics related to goods and services.

3. Classification of Individual Consumption by Purpose (COICOP)

It is used to define both the individual consumption and expenditure on one hand, and the individual consumption only on the the other hand.

4. Classification of Functions of Government (COFOG)

Developed by the OECD, It classifies government expenditure data from the System of National Accounts by the purpose for which the funds are used, which helps the analysts and the government entitiies‘ monitor evaluators in evaluating the governmental expenditure effeciency.

5. Balance of Payments Manual (sixth edition)

The Balance of Payments Manual (sixth edition), which is prepared by the International Monetary Fund, is one of the most important statistical systems that is used within the National Accounts System 2008. The accounts of the outside world sector within the National Accounts System is considered the linking point between the two systems. The two systems are similar in that they both include the same recommendations either to view accounts or to record and evaluate transactions.

Third stage: Organization

It is the last stage of preparation stages that precedes the process of data collection. The work procedures required for the preparation of this bullein have been prepared in this stage. They will begin from the next stag“collection stage" and will end with the “Evaluation stage”. In addition, the procedures are organized and collected and thier appropriate order is determined in order to reach a methodology that achieves the objectives of the National Accounts Statistics. These procedures were also described and documented to facilitate the updates in the future cycles. Furthermore, the statistical work procedures were tested to ensure that they meet the requirements of the preparation of the National Accounts Statistics in its final form. Then, the procedures of the statistical work are approved, and the road map of the implementation is developed.

Fourth stage: Data collection

GASTAT has coordinated with governmental entities and establishments that are concerned with the national accounts to obtain data for the National Accounts Bulletin. It relies on the administrative records which have been mentioned in the design stage. These records are already saved on GASTAT databases. They have been audited and revised in accordance with the scientific statistical approach and the familiar quality standards.

Fifth stage: Disaggregation of data

During this stage, raw data are disaggregated based on the classification and coding inputs completed during the data collection process, according to, The National Classification of Economic Activities ISIC4, The Central Products Classification CPC2, The Classification of Functions of Government COFOG, The Classification of Individual Consumption by Purpose COICOP, in addition to the Balance of Payment Manual (6th edition). The data of the National Accounts Bulletin are illustrated in appropriate tables to ficilitate summarizing and understanding them, extracting the results, comparing them with other data, and referring to them easily.

During this stage, data are processed by going through many steps such as:

First: Data logicality and comprehensiveness:

To ensure quality and accuracy of the bulletin’s statistics, all the data are reviewed and matched to check their correctness and accuracy in a way that fits the nature of such data. Data of the current round are matched with the data of the previous round to ensure their validity and logicality before processing, extracting, and reviewing the results in the next stages of data disaggregation.

Second: Data Confidentiality:

Data are kept confidential at the General Authority for Statistics. They are used for statistical purposes only. The published data come in the form of aggregate statistical tables with a number of variables that are related to national accounts.

Sixth stage: Revision

First: Data Outputs Validation:

After revising the register-based data and checking thier validity during the fourth, GASTAT started calculating, extracting, downloading the outputs, and save them on the database. Final revision operations have been done by specialists of the national accounts department by using modern techniques and software that are designed specially for this purpose.

Second: Dealing with confidential data:

According to the Royal Decree No. 23 dated 07-12-1397, data must always be kept confidential, and must be used by GASTAT for statistical purposes only. Therefore, data are protected in the data servers of GASTAT.

Seventh stage: Publication

First: Preparation and Process of the Results Designed for Publishing:

During this stage, GASTAT coordinated, organized, and revised the administrative records‘ data included in the buletin. Publishing tables and charts of data and indicators have been prepared, in addition to the metadata and methodology. They have been written in Arabic and English languages.

Second: Preparation of media material and announcement of release date:

The bulletin release date has been published on GASTAT official website at the beginning of this year. Therefore, GASTAT is now preparing the media material for the bulletin release announcement through all means of media and social media platforms. It will be published firstly on the official website with different formats including Excel format.

In this way, all clients and those who are interested in the statistics of national accounts may get access to these data easily.

Third: Communicating with cliets and providing them with the bulletin:

One of GASTAT’s objectives is to better meet its clients' needs, so it immediately provides them with the bulletin’s results once the National Accounts Bulletin is published. It also receives questions and inquiries of the clients about the Bulletin and its results through various contact channels, such as:

- GASTAT’s official website www.stats.gov.sa

- GASTAT’s official e-mail address info@stats.gov.sa

- Client Support’s e-mail address cs@stats.gov.sa

- Official visits to GASTAT’s official head office in Riyadh or one of its branches in Saudi Arabia.

- Official letters.

- Statistical helpline (920020081)

Fourth: Preservation of published content:

The Bulletin’s data are preserved and archived by Documents and Archives Center at GASTAT to be used as a reference at any time. GASTAT carried out this step to preserve such data electronically to be used again when needed.

Eighth stage: Evaluation

All GASTAT’s clients who used the results of the Bulletin will be contacted again in order to assess the entire statistical process. This is done for improvement purposes in order to obtain high-quality data. The improvements include: methodologies, procedures and systems, statisticians’ skill level, as well as statistical work frameworks. This stage is done in collaboration with data users and GASTAT clients according to the following steps:

First: Collection of measurable evaluation Inputs

The most important comments and notes are collected and documented from their sources at different stages such as the comments written by specialists who are responsible for reviewing, auditing, and analysing data collected from the administrative records. Moreover, comments and notes collected and documented by data users after being published are also collected and documented, in addition to the comments on social media and the clients’ feedback received by GASTAT through its main channels.

Second: the procedure of evaluation

The evaluation is done by analyzing the collected evaluation inputs,and comparing the results of this analysis with the ones expected previously. Therefore, a number of possible improvements and solutions are identified and discussed with specialists, experts, and concerned partners. During this step, clients' performances and satisfaction levels of using the results of national accounts statistics are measured. It is worth mentioning that based on these procedures, the recommendations for obtaining high quality data for the next national accounts bulletins are agreed upon.

Ninth stage: Management

It is a comprehensive stage required to carry out each stage of the National Accounts Bulletin production. During this stage, the plan of production is developed, which includes the feasibility study, risk management, financing methods, in addition to expenditure mechanisms. The plan also covers the development of performance indicators, quality criteria, and manpower map required for production. Through this plan, the implementation process of the tasks assigned to different departments at each stage will be followed up and reported to ensure that GASTAT meets its clients’ requirements.